Sales

Available Mon. – Fri.

9:00 AM - 7:00 PM EST

Request a Callback

Running a business today means you need a credit card processor that is quick, reliable, and secure. Choosing the right one isn’t always simple. Many business owners face challenges with hidden fees, unclear terms, and systems that won’t integrate with their business.

If you choose the wrong credit card processor, it can slow down checkouts, lead to frustrated customers, and result in lost revenue. That’s why understanding how credit card processing works is so important.

This guide will walk you through the basics of credit card processing, so you know exactly who to trust.

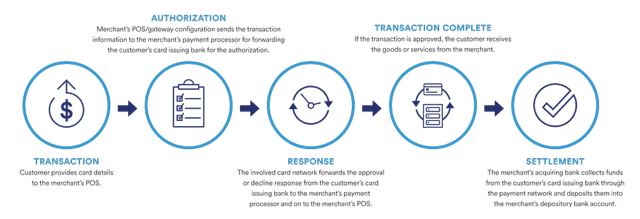

When you think of a credit card transaction, you may think of a scenario like this: a customer wants to purchase something from your business, so they use their credit card. Once the customer swipes, taps, or inserts their credit card, a whole system unfolds behind the scenes.

There are multiple participants involved in the transaction, each with an important role in transferring the money from your customer's account to your bank account.

We’ll take a closer look at the role each participant plays and explain how understanding credit card processing gives your business an advantage over your competitors. As a credit card processing company, Elavon has years of experience with credit card transactions and can help your business understand how each step works.

Without credit card processing, your customers wouldn’t be able to purchase your goods or services, and you could lose revenue. Rather than losing a sale when customers don’t have cash, you can make payments easy with a credit card processor. It can boost sales, expand your business’s reach with online and mobile payments, and allow for secure payment options.

Additionally, accepting credit cards means your customers can pay for larger purchases, so you can complete more sales.

Every transaction made requires an entire chain of participants, ensuring the process is seamless. Here’s every participant involved:

Without every participant, transactions would fail, and you would lose sales. See how Elavon’s merchant services and payment gateways work.

Although credit cards are one of the most common forms of payment*, there are other ways customers can pay. They expect your business to accept multiple payment options. This ensures you make more sales while keeping customers happy.

Other common payment options include:

Offering these three types of credit card acceptance options helps your business meet customers’ expectations and makes it easier for them to buy from you. The three types include in-person, online, and mobile payments.

Payment types vary in how they work, the benefits they offer, and the situations they are best suited for. Understanding how each payment acceptance method works can help you select the most suitable solutions for your business and customers.

When you’re ready to start accepting credit card payments, you’ll need a credit card terminal or point-of-sale system, which allows your customers to use their credit cards to make the necessary payment.

Modern POS systems go beyond swiping a card. They accept contactless payment methods such as Apple Pay, Android Pay, and Samsung Pay, so your customers can pay the way they want.

Before you can start accepting credit card payments, you’ll need a merchant account that connects your payment processor to your business bank account. From there, you’ll install your POS hardware or software, train your employees, and run diagnostic transactions to ensure a seamless checkout.

Now that you know the credit card process, it’s time to choose a processor. Some may seem trustworthy at first, but once you sign a contract, they can charge hidden fees or include unclear terms. Ensure you read all the contract’s fine print before signing. It’s important to choose a credit card processor that is transparent, dependable, and works well with your business.

There isn’t just one cost for credit card processing. Often, it varies depending on the card types accepted and the manner in which those payments are accepted. Understanding these fees can help you avoid high-cost surprises when you choose a processor.

The three common types of fees include:

Other credit card processors may charge additional fees, including a one-time setup fee. If you know the details of each type of fee, you can more effectively choose the right provider that fits your business preferences.

With Elavon, you can accept payments in person starting at 2.60% + 10¢ per qualified swipe or chip transaction. For online payment acceptance, rates start at 2.90% + 30¢ per qualified transaction. For more information about the cost of Elavon’s credit card processing, click here.

More people are using their mobile devices to make purchases.* Accept Near Field Communication (NFC) mobile payments such as Apple Pay or Google Pay.

These payments are faster than normal credit cards. Mobile payments occur almost instantaneously as the customer places their mobile device hovering above the POS system to make their purchase.

Does the credit card processor handle the types of transactions your industry requires? Not all processors can support your business or industry type. Choose the one that can.

Here are the industry-specific transactions Elavon supports:

Elavon works with a wide range of businesses across many industries. Depending on your industry, it’s important to choose a credit card processor tailored to your business needs.

A credit card processor wants your business to trust them as a reputable partner, which means keeping all payment transaction data safeguarded.. Payment data security should be your top priority when it comes to choosing a credit card processor.

All businesses that accept card payments must validate and comply with the Payment Card Industry Data Security Standard (PCI DSS). These standards cover rigorous practices and requirements for processing, storing, and transmitting card data via payments, devices, and e-commerce websites, ultimately protecting both customers and merchants.

PCI DSS requirements help protect card payments from fraud and cyber threats, keeping transactions as safe as possible.

Critical ways credit card processors can help merchants protect payment data:

Visit Elavon’s PCI DSS Compliance page here for more information.

Credit card processing is a necessity for modern businesses, offering numerous benefits. From faster transactions to advanced security, efficient credit card processing provides you with the tools to stay competitive, such as:

Taking the risk of a poor payment processor results in many negative consequences that can hit your business hard, including:

Lost sales:

If your current payment system is slow and unreliable, customers are less likely to make a purchase, causing you to lose sales.

Frustrated customers:

Long checkout lines and declined transactions can lead to frustrated customers, which may hurt your reputation.

Security breaches and fraud:

Weak or outdated payment systems increase the risk of accepting stolen payment data or loss of payment data leading to fraudulent transaction liability, card brand fines, fees or assessments and other legal or regulatory issues. Keep your customers’ data protected with advanced data security solutions available through your credit card processor.

Slow or inconsistent cash flow:

Delays in your payment settling and funding can affect paying your staff, bills, and investments. A processor should support your business’s growth.

Business inefficiency:

Manually inputting a customer’s card or trying to fix an incompatible system can waste your time. This ultimately creates errors and potential complications in the future.

Difficulty switching processors later:

A processor that locks you into a bad system or long-term contract makes it harder to upgrade or switch to a better solution later.

If you realize that you're paying way more for credit card processing than you expected, it may be time to switch processors. When you switch to a new processor, make sure it aligns with your business’s goals and will not keep you in the dark. Make the switch and start saving on transaction fees.

Follow these steps if you want to switch processors:

Elavon can answer any additional questions you have about switching from your current processor here.

Setting up credit card processing doesn’t have to be difficult. Many processors allow businesses to accept payments across in-person, online, and mobile channels.

Your business needs a credit card processor that will be with you every step of the way. Some providers let you sign up without talking to anyone, which may seem nice, but the minute you have a problem, they’re not there to help.

A good credit card processor will offer clear guidance, reliability, and easy setup methods. They should be helping you through the entire process and beyond.

Here are the basic steps to setting up credit card processing:

Customers need to know that they can trust your business. They’re not just buying a product or service from you.

Instead, they want to have a positive experience with your business. You can offer them that by making the payment process easy. Efficient credit card processing helps ensure quick checkouts, which creates a better experience for your customers.

Customers will judge your business based on how seamless your checkout process is. Accepting credit cards not only builds trust but also offers flexibility and convenience. Give your customers a positive checkout experience, so they’ll be more than happy to come back.

Accepting credit cards means your customers can:

Understanding credit card processing means you know how transactions work and how to give your customers a consistent, dependable payment experience. With credit card processing, your business will continue to grow. We recommend choosing the right processor to help build customer trust, protect their data, and boost overall sales. Because every transaction matters.

To learn more about how Elavon can support your business with credit card processing, start here.

Elavon is proud to be a recognized leader in the payments industry by Forbes Best of 2024 as one of the 10 best credit card processing companies.

We are your trusted partner for all of your payments needs. Don't just take it from us – see what others are saying on Trustpilot.